�������ߣ���¡�㾫��������

�������ϻ�����ҵ��MLP���ܲ�����ע������MLPģʽ�ǻ�����۵ģ���ѭ���ԣ�

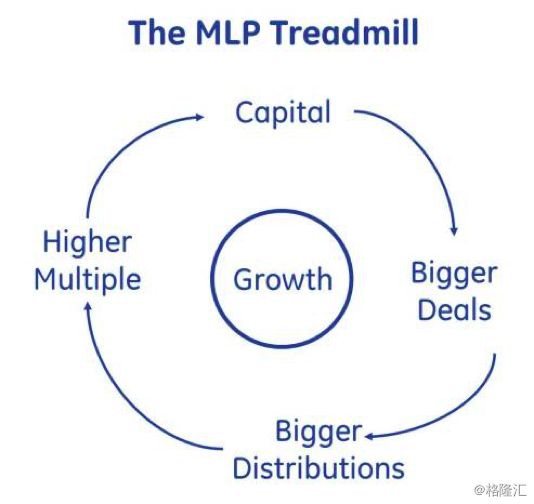

����We arrive at a situation where an incentivefor risky growth is then combined with a reliance on outside funding. Itis this dynamic that leads to the MLP Treadmill.

�����������������Ķ����Ͷ��ⲿ�ʽ�������������һ���������ֶ�����MLP��˾�������ܲ����ϡ�

����MLPs constantly need more capital to drivebigger and bigger deals so that they can keep growing distributions. Inturn, bigger distributions will lead to a higher valuation. This is theMLP Treadmill. Once you get on and start feeding growth through externalfunding, it is very hard to stop and get off. And get off you must,eventually.

����MLP��˾��ҪԴԴ���ϵ��ʽ�Ͷ���������Ŀ�У��Դ���߷ֺ죬���ߵķֺ췴������������ߵļ�ֵ�������MLP�ܲ�����һ����̤��ȥ����ʼ���ⲿ�ʽ�Ͷ�ʴٽ��������ͺ���ͣ����Ȼ�����������������ջ��ǵô���������

����One of the inherent contradictions of theMLP model is that, if it works exactly as designed, the company will hit the high splits quickly. As the GP grabs a biggerand bigger piece of the pie, the cost of capital will increase commensurately. As one observer put it: �� The Company��s unitprice depended upon constantly increasing dividend distribution, andever-higher dividends, creating ever-greater IDRs, required staggeringinfusions of capital.��

����MLPģʽ���е�ì��֮һ�����������ƺõľ籾�ߣ���������������ֵ��Ǹ��㡣����ͨ�ϻ��˵ķݶ�Խ��Խ���ʱ��ɱ�Ҳ��ͬ�����ӡ�һ���۲�Ա����˵������˾�Ĺɼ�ȡ���ڲ������ӵķֺ��ȣ�Խ�ߵķֺ��ܴ���Խ��IDRȨ������Ҫ��������ʡ���

����For example, below is a look at the 20 yearlifespan of an MLP. We have assumed a 7% yield at the outsetwith an expectation that the yield will grow by 3% per year. Theseassumptions give the MLP an initial cost of capital of 7%. But, by year20, the GP is taking 4q% of distributable cash flow and the MLP must earn 51%on its equity to preserve the distribution growth to LPs. The universeof investments providing that sort of return is rather small.

�������磺������ʾ��һ��MLP��ҵ20�����ҵ�������ڡ����Ǽ����ʼ��������7%��Ԥ��������ÿ�갴3%����������Щ�����£�MLP��ҵ�ij�ʼ�ɱ�ռ���ʱ���7%�������ڵ�20��ʱ����ͨ�ϻ������߿ɷ����ֽ�����4%��MLP��ҵ�������ù�Ȩ��51%�Ա�֤���ϻ��˷ֺ�����������ܹ��ṩ��˸ر���Ͷ����ʮ���ٵġ�

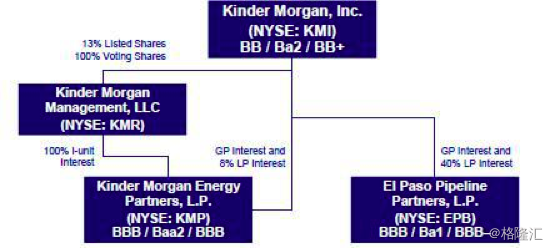

����Kinder Morgan serves as a cautionary tale. Kinder Morgan rode the MLP Treadmill all the way to its logicalconclusion. From 1990 to December 1996, Richard Kinder served as thePresident and COO of Enron Corporation. He resigned from Enron in 1996 afterbeing denied a promotion to CEO. He had a headstrong belief in theprofitability of collecting a toll to move energy through pipelines�� which didnot gibe with the more aggressive vision at Enron. After leaving Enron,he and college friend William V. Morgan started a pipeline business. They firstpurchased Enron Liquids Pipeline, a natural gas conduit business that Enron waseager to get rid of, for $40 million. They also merged with KNEnergy. After a number of acquisitions, most prominently El PasoCorporation, Kinder Morgan became the largest midstream energycompany in North America. Enron declared bankruptcy in 2002.

�������Ħ����˾���Ǹ���ʾ���档���Ħ����MLP�ܲ�����һֱ�����ܣ����Ľ��Ҳ������֮�С���1990�굽1996��12�£������·��µ��ΰ�Ȼ��˾�������������ۺ�����Ȼ���͵�����˾֮һ������ϯ��Ӫ�١�1996�����CEOʧ�ܺ����Ӱ�Ȼ��˾��ְ�����ᶨ����Ϊ�Թܵ�����ʯ����ȡ������������ͼ�ġ��뿪��Ȼ֮�������������� V·Ħ����ʼ�˹ܵ���������⡣����������4000���������°�Ȼʯ�����乫˾�����ǰ�Ȼ��˾ʮ������ѵĸ�����Ȼ���ܵ�ҵ����ӹ�˾�����ǻ���KN��Դ��˾�ϲ����������Ħ��ͨ��һϵ�еĺϲ��������Ǹ�����������˾�ĺϲ�������˱�������������Դ��˾����Ȼ��2002�������Ʋ���

����By 2014, the Kinder Morgan empire hadgreatly expanded.

����2014��ʱ�����Ħ���۹��Ѿ�����������ˡ�

����Enron Liquids Pipeline evolved into KinderMorgan Partners (KMP), a master limited partnership. KMP earned themajority of its income by transporting oil, natural gas and CO?through its approximately 52,000 miles of pipelines located throughout theUnited States and Canada. It also owns approximately 180 terminals dedicated tohandling natural resources. The Company owns the physical pipelines, andcollects lucrative fees when natural resource companies use those pipelines totransport their products. KMP had increased its dividend every quartersince its inception.

������Ȼʯ�ܵ���˾����˽��Ħ���ĺϻ��ˣ�KMP������ҵ���������κϻ���ҵ��KMP��ӯ���������ڱ鲼ȫ�������ô�Ľ�52000Ӣ��Ĺܵ���ʯ�͡���Ȼ���Ͷ�����̼�������䡣ͬʱ������ӵ��180���յ�վ�Դ�����Ȼ��Դ����˾ӵ��ʵ��Ĺܵ�������Դ��˾������ܵ������Ʒʱ����˾������ȡ��������KMP��һ��ʼ��ʵ����ÿ���ȵķֺ�������

����Combined, the Kinder Morgan family was thethird largest energy company in North America, with an estimated combinedenterprise value of ~$140 billion. Among other assets, the Kinder Morganfamily owned the largest natural gas network in North America.

�����ϲ�֮��Ľ��Ħ����˾�DZ���������Դ��ҵ����ҵ��ֵ����Ϊ1400����Ԫ���������ʲ����ԣ����Ħ��ĸ��˾ӵ�б���������Ȼ�����硣

����Yet on August 10, 2014, Kinder Morganannounced that it was shutting down its MLP and rolling them up into the mainpublic company. Why would they do this?

����Ȼ����2014��8��10�ţ����Ħ�������ر�MLP��˾�ع鵽��Ҫ�����й�˾�ΪʲôҪ��������

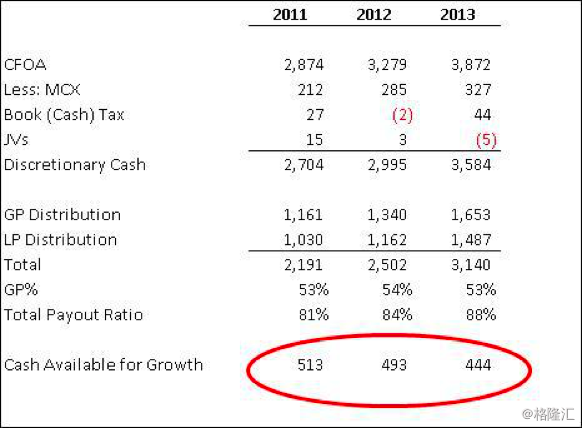

����By 2011, its MLP, Kinder Morgan Partners(KMP), was in the high splits. The GP was earning more than 50% of totaldistributions to unit holders. Further, over 100% of cash not neededimmediately by the business was being distributed out. How much did thisleave for growth investments? Not a whole lot:

������2011��ʱ�����Ħ����MLP��˾��Ҳ�����Ħ���ϻ﹫˾���ʹ��ڸ߷�λ�㡣��ͨ�ϻ������÷ֺ���ڵ�λ���кϻ������÷ֺ��50%�����ߣ���˾��ʱ����Ҫ���ϵ��ֽ�100%��������ˡ�����һ����Ͷ��������������Ǯ��ʣ�����أ���Ȼ��ʣ����

����Kinder Morgan Partners, Discretionary CashFlows, 2011-2013

����

����Source: Company filings via Sentieo.com

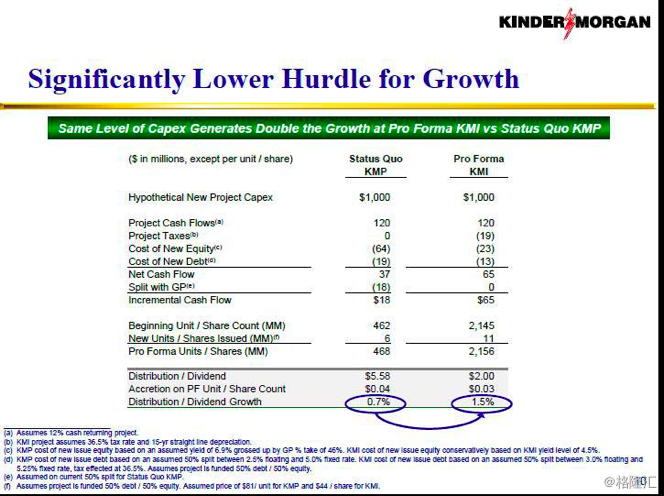

����Further, with the GP in the high splits, theMLPs cost of capital was enormous and the corresponding hurdle rate for newinvestments severely limited the universe of accretive investments. Hereis a slide from a Kinder Morgan investor presentation showing the return tominority unitholders and shareholders from a new investment in the MLPstructure and in the more traditional corporate structure:

�������ߣ�����ͨͶ���߷ֺ�϶�ʱ��MLP��ҵ���ʱ��ɱ��ܸ߰�����Ӧ����Ͷ����Ŀ��Ҫ��ر����������ۼ�Ͷ�ʡ�������ʾ�����Ħ��Ͷ���߹�ϵչʾPPT�ֱ�չʾ����MLPģʽ���Ϊ��ͳ�Ĺ�˾��������λ����֤ȯ�������ɶ��õ��Ļر���

����

����Kinder Morgan opted to hop off the MLPTreadmill rather than extend the pain. In 2014, they rolled up their MLPsinto the Sponsor, effectively reversing years of drop downs.

�������Ħ��ѡ������MLP�ܲ�������ʹ�ࡣ2014��ʱ�����ǰ�MLP��ҵ�����������̣��Ӷ���Ч��Ť��Ϊӯ��

����Conflicts of Interest

���������ͻ

����When we take a minority position inpublically traded companies, we always face the risk that the business is beingrun for the benefit of the majority owner and to the detriment of minorityowners. However, this risk is dramatically heightened if none of thetraditional protections for minority ownership are in place. Such is thecase with MLPs

����һ�����dz����������й�˾�Ĺɷݣ����ǻᾭ�����ٹ�˾���С�ɶ�����Ϊ��ɶ�ı���������һ��С�ɶ�û�д�ͳ������ʩ�����ַ��ջ����ؼ�ǿ��MLP��ҵ����ˡ�

����a. FiduciaryDuty Waived

���������������

����As discussed above, MLPs are organized aslimited partnerships rather than the more common corporation. MLPs takefull advantage of the fact that Delaware law does not require GPs to act in thebest interests of the LP. Therefore, as shocking as this sounds, the GPmay act free of any duty or obligation to the MLP or its limited partners. Forexample, the PBFX 10-K states: ��Our general partner and its affiliates,including PBF Energy, have conflicts of interest with us and limited fiduciaryduties to us and our unitholders, and they may favor their owninterests to the detriment of us and our other common unitholders.��(emphasis added) This provision alone is enough to scare us away fromMLPs

��������֮ǰ�����ģ�MLP��ҵ��ȡ�����������κϻ��ƣ������ͨ�Ĺ�˾�Ʋ�һ����MLP��ҵ�ܺõ���������������˾����Ҫ����ͨ�ϻ���Ϊ���ϻ��˵��������Ĺ涨����ˣ��������������������ţ���ͨ�ϻ��˶�MLP��˾�����������ϻ��˸�������Ҫ�е��κ����λ��������磬PBFX���걨������˵�������ǵ���ͨ�ϻ��˼���ϻ﹫˾������PBF��Դ��˾��ͬ�ҷ��������ͻ�����ҷ�����λ���г�֤ȯ�����߳е������������Ρ����п��������ҷ������ҷ�������ͨ��λ����֤ȯ�����ߵ��������������������档�����ٴ�ǿ�������������������������Ƕ�MLP��ҵ����ȴ����

����b. IDRsMean That Deals Can Be Accretive To The GP And Not The LP

����IDR(��������Ȩ��)��ζ����ͨ�ϻ��˿����ܽ�����ֵ�ԣ��������ϻ������ܲ�����

����The way IDRs are calculated makes itpossible for actions to be taken that are accretive to the GP but notnecessarily to existing LPs. Distributions paid to the GP are not based on thedistribution per LP unit but the gross distribution to LPs. Therefore,even if the distribution per unit remains the same, the GP will receive agreater distribution. Here is a simplified example:

����IDR��õķ�ʽ����ͨͶ���ߵ��Բ�ȡ�ж������ֵ�ر������Ƕ����е�����Ͷ������˵������ˡ���ͨ�ϻ��˻�õķֺ첢�ǻ������ϻ��˻�õķֺ죬���ǻ����������ϻ��˵��ֺܷ����á���ˣ���ʹÿ����λ�ֺ���һ������ͨ�ϻ��˻������õ�����ķֺ졣�и������ӣ�

����Notice that the equity funded acquisition,results in a 10% increase in the distribution to the GP while the LP remainsthe same.

���������Ȩ�����չ���ʹ��ͨ�ϻ��˵ķֺ����ӣ������ϻ��˵ı��ֲ��䡣

����c. DropDowns Are Not At Arms-Length

�����µ����ǹ�ƽ��

����Drop downs are often touted as a benefit ofMLPs. For example, the amount of assets available for drop down by theSponsor is used as a rough proxy for the future growth of the MLP. But,drop downs create a terrible conflict of interest. How can aminority owner of the MLP have any assurance that both parties are negotiatinga fair deal?

�����ɼ��µ���������������MLP��ҵ���ܵ��洦�����磬�������ṩ��֧���µ����ʲ������������ٽ�MLP��ҵδ�������Ĵ������Ʒ�������µ�����˷dz����ص������ͻ��MLP��ҵ��С�ɶ�����ܱ�֤˫����Э�̳�һ����ƽ�Ľ����ء�

����d. Lackof Voting Rights

����û��ͶƱȨ

����Unlike common shareholders, MLP LPs haveseverely restricted voting rights and no vote for the board of directors.

��������ͨ�ɶ���ͬ��MLP���ϻ��˵�ͶƱȨ���ر����ƣ����»����û��ͶƱȨ��

����Other Ways Management Can Rip You Off

������������ƭ��������ķ�ʽ

����Management has several other ways it can ripoff the minority owners

����������Ҳ��ͨ������һЩ������ƭС�ɶ�.

����1. AccountingGames

����������Ϸ

����The most straightforward method managementhas to rip off investors is playing games with the numbers. As statedearlier, MLPs are required to distribute all available cash. However, allavailable cash is not a term defined under GAAP. This gives managementsignificant leeway to pump up the numbers.

������������ƭͶ���ߵ���ֱ�ӵİ취���������������¡� ��������������˵��MLP��ҵ��������еĿ�֧���ֽ�����ȥ���������п�֧���ֽ�GAAP�����������ȷ�����һ���������˹�����ܶ����ȥ�����������¡�

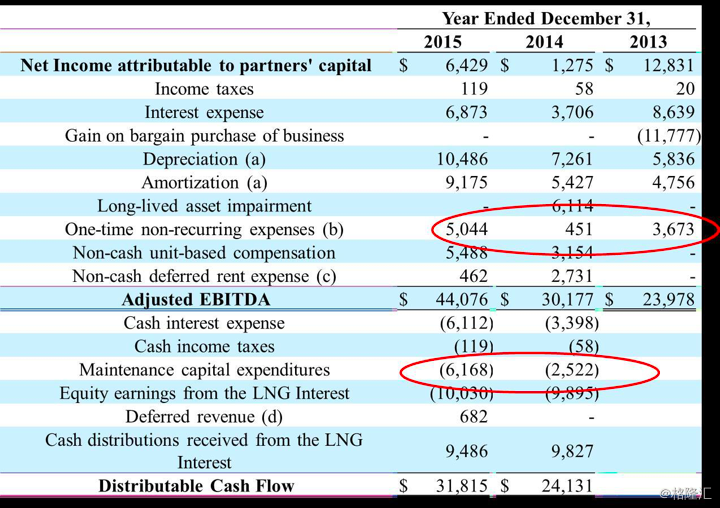

����Below is a typical calculation of distributablecash flow by an MLP.

����������һ��MLP��˾���͵ļ��������֧���ֽ�ķ�ʽ��

����Source: ARCX 10-K

����A couple of items stick out. First,the ��one-time non-recurring�� expenses sure do seem to recur a lot. Buteven more importantly, they are true expenses and a reduction to cash. Why are they being added back?

�����м����������Ŀ�������ǡ�һ���ԷǾ����ԡ�����ȷʵ�������֡�������Ҫ�������Ƕ���ʵ��ʵ�Ļ������Ƕ��ֽ�����ģ�Ϊʲô�ֱ����˻�����

����Second, ��maintenance capital expenditures��is not a term defined under GAAP. This gives management a lot of leewayto play around with the numbers. Per the 10-K, management simply definesmaintenance capital expenditures as ��(i) clean, inspect and repair storagetanks; (ii) clean and paint tank exteriors; (iii) inspect and upgradevapor recovery/combustion units; (iv) upgrade fire protection systems;(v) evaluate certain facilities regulatory programs; (vi) inspect andrepair cathodic protection systems; (vii) inspect and repair tankinfrastructure; and (viii) make other general facility repairs asrequired.�� This last point is vague enough to cover (in good years) ornot cover (in bad years) just about any capital expenditure.

�����ڶ�����ά���ʱ�֧����Ҳ����GAAP���������ȷ�ж��������������ܴ�ռ���Ū������Ϸ��ÿһ���걨�У������㶼�����ض�ά���ʱ���֧���������Ķ��壺��(i) ��ࡢ��顢�������ޣ�(ii) ���ͷ�ˢ�ޱ��棻(iii)��������������պ�ȼ���飻(iv)������������ϵͳ��(vi) ��������������ϵͳ��(vii)������������ʩ��(viii)��Ҫ����������ʩ���� ����ģ�����㹻���ǵ��������治���������κ��ʱ���֧�����߲���������������������Щ�ʱ���֧��

����Maintenance Capex, however, is intended torepresent the cost inherent in maintaining the Company��s current capacity, andis generally funded from operating revenues. Because of that, expendituresclassified as Maintenance Capex reduce the funds that may be distributed to thegeneral partner and the unitholders. The GP has a powerful incentive toclassify whatever expenses possible as Expansion Capex, as that leads to alarger payment for the GP.

��������ά��Ԥ�㱾����ά����˾�������������Ŀ�֧����Ӧ����������Ӫ���롣��ˣ�������ά��Ԥ��ijɱ�Ӧ�ü�ȥ���÷������ͨ�ϻ��˺͵�λ����֤ȯ�����˵��ֽ���ͨ�ϻ�����ǿ��Ķ�����һ�л����������ܹ���Ϊά��Ԥ�㣬���������ָ���ͨ�ϻ��˵��������ߡ�

����Depreciation, depletion and amortization(��DD&A��) costs��reflective as they are of the anticipated expense ofmaintaining assets��should roughly mirror Maintenance Capex. Defying logic, theMLPs we looked at all had Maintenance Capex amounts far lower than theirDD&A. In fact, the average ratio in 2015 was just 30%.

�����۾ɣ���ģ�̯������(��DD&A��)������ӳ��Ԥ�ڵ��ʲ�ά���á���ά��Ԥ�ڴ��³����ȡ����ǹ۲쵽��MLP��ҵ�����ϴ�������ά��Ԥ�ڷ��ö�ԶԶ����DD&A���á���ʵ�ϣ�2015���ƽ�����ʲŵ�30%��

����2. LongTerm Contracts can mask deteriorating economics.

����1. ���ں�Լ�����ڸǾ���˥������

����One of the strengths of MLPs is therelong-term contracts. This gives investors visibility far into the futureand makes projecting future cash flows easier and more reliable. It alsogives the business financial stability. But, long term contracts are atwo-edged sword. Sure, it��s great to have the predictability, but whathappens when the contract ends? Will the MLP be able to negotiate a renewalon same or better terms or will the customer walk away altogether? Longterm contracts can paper over deteriorating economics until investors get arude awakening. Particularly in a business as cyclical as oil and gas,future economics can look far different than the present.

����MLP��ҵ������֮һ���dz��ں�Լ��Ͷ���߿��Խ�˶���δ����Ҳ�ɸ����㡢���ɿ��ض�δ���ֽ�����ʹ��������мƻ������ں�ͬҲ����ҵ�ڲ����ϸ����Ƚ������dz��ں�ͬ�ǰ�˫�н�����Ȼ���п�Ԥ�����Ǽ��õģ�����һ����ͬ���ڻ������أ�MLP��ҵ����Э����ǩͬ�����������ǩ�¸��õ������𣿻����п�����ʧ�����еĿͻ��أ����ں�ͬ�����ڸ�ס�»��ľ��ã�ֱ������Ͷ���߲Ż�Ȼ����������������������������ҵ�δ���ľ���״�����ܺ����������ͬ��

����3. MidstreamCompanies Still have Commodity Exposure

����3�����ε���ҵ�������Ŵ�����Ʒ��Ӱ��

����While it is certainly true that midstreamcompanies do not have direct exposure to commodity pricing, the commodity cyclestill impacts their business. For example, storage businesses do better whenforward prices are higher than current spot rates, a situation known as��contango.�� Contango increases storage needs because oil companies knowthey get more money by waiting than by selling it immediately. The GP hasfiduciary duty first and foremost to its own shareholders, not to the LPs.Because the GP has almost complete control of the MLP in any decision makingprocess, the GP can maximize its own benefits ahead of or even to the detrimentof the LP.

������ȷ�����ε���ҵ��������Ʒ�ļ۸���ֱ�ӹ�ϵ�����Ǵ�����Ʒ����������Ȼ������ҵ��Ӱ�졣���磬���ڻ��۸���ڵ�ǰ����ˮƽʱ���洢����������ģ����������Ϊ���ڻ���������ڻ����̧���˴洢������Ϊʯ��˾�˽ⰴ������������������Ǯ����ͨ�ϻ�������Ҫ�������Σ�����Ҫ���Ƕ��Լ��Ĺɶ������Ƕ����ϻ�����������Ρ���Ϊ��ͨ�ϻ��˶�MLP��ҵ�����о��߹��̼�������ȫ�Ŀ���Ȩ��������ͨ�ϻ��˿��Խ��Լ������������λ�����������������ϻ��˵�����Ϊ���ۡ�

����A Closer Look At WPT

����������۲�WPT��World Point Terminals��

����While combing through the wreckage of theMLP sector, we did come across one company that looks pretty good, WPT:

����������MLP�IJк����ij���Ѱ�����ڷ�����һ�ҿ���ȥ��������ҵ��WPT��

����Most importantly, WPT management seems toreject the idea of hopping on the MLP Treadmill. It has never increasedits distribution. It has distributed the minimum quarterly dividend eachquarter since going public in August 2013. Because the distribution hasnot grown, the company has not triggered any distributions on the IDRs. Further, it has not taken any debt to fund growth investments and has onlyparticipated in one dropdown transaction.

��������Ҫ����WPT�Ĺ������ƺ���̫Ը������MLP���ܲ���������δ��߹��ֺ죬��2013������һ������һֱ�ڰ���ͼ��ȹ�Ϣ�ֺ졣���ڷֺ첢δ���ӣ��ù�˾��δͨ��IDRs�����ֺ졣���ߣ���Ҳ��δͨ����ծ��������Ͷ�ʣ����·Ž��ס���ע��ĸ��˾����Ŀ�ƽ���MLP��ҵ�У�Ҳֻ�����һ�Ρ�

����As one might expect, Wall Street is nothappy about this. On the Q4 2014 conference, the following exchange tookplace:

�����������ϣ������ֶԴ˲���ϲ���ּ�����2014��Q4�ĵ绰�����ϣ��������������飺

����Eric Wolff, Hawk Ridge Partners �C Analyst

���������·�ֶ���ӥ��ϻ��ˡ����о�Ա

����I appreciate the conservative nature of thebalance sheet. At the same time, I think your business is relatively stable,and one could argue that a very, very modest amount of debt, even if it��s justone or two times, is exceptionally safe, given the stability of the assetshistorically. What��s been the aversion to even taking on a modest amount ofdebt?

�����Һ������ʲ���ծ������ʵ���ͬʱ������Ϊ��˾�����˵���Ƚ��ģ����ǵ���˾�ʲ�������ƽ���ԣ�һ�������������͵�ծ��ˮƽ�����쳣��ȫ�ġ�Ϊ�ι�˾��Ը������ʵ���ծ���أ�

����J.Q. Affleck, World Point Terminals, LP �C VPand CFO

����J.Q.�������ˣ�World Point Terminals, ���ϻ��ˡ�����ϯ��CFO

����Well, I think that��s kind of been a messagefrom our Board that we do like operate in a very conservative nature. I thinkthere��s a premium on having some flexibility in the business. As you��ve seenthe capital markets kind of freeze up for MLPs, we feel like we��re in a verystrong position to have the access to the funding through our debt facility asopposed to maybe being at that one or two times level that you speak of, andthen having to access the capital markets if we wanted to maintain that ratio.So I think it��s just kind of the conservative and flexibility aspect that we��vebeen looking at to provide that opportunity for us.

�����õģ�����Ϊ��˾ƫ�ñ�����Ӫʵ���Ƕ��»ᴫ�������Ҿ�����ҵ���������ϻ��з�չ�ռ䡣�����������ʱ��г���MLP��ҵ����������Ƕ����ˣ����Ǿ��ù�˾�ڽ�ծ���ʷ����λǿ����������˵��һ��������ծ��ˮƽǡ���෴�����DZ�������ʱ��г���ά��������ʡ���������ֻ��ϣ���Ա��ء����ķ�ʽ����ȡ���ᡣ

����Nevertheless, an investment in WPT takes alot of faith in management.

����������ˣ�WPT��ÿһ��Ͷ�ʶ���Ҫ������ǿ������

����For example, the sponsor, Apex Oil Company,is not public. As a result, you must accept management��s assertions thatthey are doing just fine. For example, on the Q4 2015 conference call,the CFO stated: ��Apex obviously does not disclose its financials, but ithas done very well during the recent market conditions, and we consider them tobe a very strong �� very strong from a credit perspective. We��re not really in aposition to disclose kind of their debt balances or any specifics with regardto their financials, but we don��t see them as posing any risk.��

�������磬������Apexʯ��˾��һ�������й�˾���������������Ź�������˵�ĸù�˾��Ӫ���á����磬2015����ļ��ȵĵ绰�����ϣ�CFO˵������Apex��Ȼû����¶�������Ϣ��������������г������﹫˾��չ���ã�������Ϊ��˾���Ŵ�������ʮ�����á����Dz���������¶��ծ��״���������κβ������ݣ�������Ϊ��˾�������κη��ա���

����Second, the Company has exercised a greatdeal of discretion in undertaking acquisitions. However, one of theirstated objectives is to grow via third party deals. How long will theywait for their fat pitch? Will they get impatient and make avalue-destroying acquisition?

������Σ���˾�ڲ������濼�ǵ�ʮ���ܵ�����Ŀ��֮һ��ϣ��ͨ�������������ٽ�����������ʲôʱ����ܵ����������ǻᰴ�Ͳ�ס���������ֵ�IJ�������

����Third, as described above, WPT and itscompetitors all assert that they have limited competition because of the uniquelocation of their assets and the lack of suitable substitutes for competitors.

��������������������WPT���侺�����ֶ����Լ����ٵľ������ޣ���Ϊ�ʲ��ж��صĵ���λ�����ƣ��Ծ������ֶ��Ժ��ʵ�����߲��ࡣ

����Nevertheless, on page 63 of the latest 10-K,WPT states: ��Despite these barriers, there has been significantnew constructionof residual fuel storage facilities along the GulfCoast in recent years, which we believe may account for some of theunutilized storage capacityat our Galveston terminal.�� (Emphasis added.) We wrote to a member of the board of directors as wellas Investor Relations seeking a reconciliation of this seemingcontradiction. We received no response.

�������������µ��걨�ϣ�WPT�ڵ�63ҳ�������������ϰ����ڣ��������д������µ�ʯ�ʹ洢��ʩ�ڸ߷�����������������Ϊ��δ�����ļӶ�ά˹����ͷ�Ĵ洢������ש���ߡ������ش�ǿ�������Ǹ����»��е�һ����Ա���Լ�Ͷ���߹�ϵ����д�ţ���ͼ��������ܵ�ì��Ѱ��ͽ⡣�������Dz�δ�յ��ظ���

����Any MLP��s management is at best a benevolentdictatorship. It has at its disposal all of the tools above. Sofar, WPT has simply chosen not to use them to a great extent.

����MLP��ҵ�Ĺ��������Ҳֻ���ʴȵĶ��üҡ������ᵽ�ķ������ɹ���ʹ�á���ĿǰΪֹ��WPTֻ�ǵ�����ѡ�����̶ȱ���ʹ����Щ������

����When The Boring Is Made Exciting, Lookout!

������Ȥ����װ����Ȥ��ҪС���ˣ�

����When operating properly, midstream companiesshould be stable and boring. They are a utility-like business that shouldbe valued like a utility. Not content with utility-like valuations, WallStreet attempted to make them more exciting. When Wall Street makes theboring look exciting, investors should hold on tight to their wallets.

����ֻҪ��Ӫ���ã����ε���ҵӦ����ƽ������Ȥ�ġ����������ڹ�����ʩ��ҵ��ҲӦ��������������ʩ��ҵ����ֵ�����ǻ����ֲ����������ù�����ʩ��ҵ������ֵ����������ϣ��������MLP��ҵ����ȥ���ԸС�������ͻȻ����Ȥ�Ķ�������Ը�ʱ��Ͷ���߾�Ҫ�ú�ץ���Լ���Ǯ���ˡ�

����As demonstrated above, the growth indistributions was not sustainable. But even with the drop in the price ofoil and the collapse in valuations, MLPs are still unattractive due to thecomplicated structure and the poor incentives it creates.

���������������ֺ�����������ǿɳ����ġ��������ͼ��µ�����ֵ������MLP��ҵ����ȥ�Ծ�û������������Ϊ���Ľṹ�ܸ��ӣ�������ļ�������Ҳ�����ơ�

����[1]Another option is to reduce thequarterly dividend. Boardwalk Pipeline Partners did just that and saw itsmarket capitalization drop by 50%.

����[1] ����һ��ѡ����ǽ���ÿ���ȵķֺ졣Boardwalk Pipeline Partners��������ֵ����50%��

����[2]It��s odd to root for a stagnantdistribution but such is the upside down world of MLPs.

����[2]��Ȼ��Ը�ֺ�ͣ�Ͳ�ǰ��Щ��֣�������MLP�����������Ҫ�ߵ�������

��¡�㣬 һ����˼��ĺ���Ͷ��ƽ̨

)

)